HOW TO START MANAGING YOUR MONEY NOW

Growing up, money wasn’t exactly a positive topic of discussion. I heard many sayings like “Money is the Root of all Evil”, which eventually turned to “LOVE of money is the Root of all Evil. Also sayings like, “Don’t count the money in my pocket” whenever I wanted my mother to buy something that seemed easy to purchase. There were also notions that the wealthy somehow weren’t as noble or God fearing because they had money. Not all of these ideas came from home, many came from hearsay on television and in politics. In contrast, I witnessed the wealthy give openly to the public as well as to my family. Needless to say, not only was I very confused about money, I believed my life would probably always be one of poverty.

I’ve racked up debt like many other people I know, and almost none of it was “irresponsible” spending. Things like, student loan debt, a car loan, credit card debt from an emergency purchase of a laptop, and basic living expenses from my move to Los Angeles. I could go more in depth, but you get the picture, I was “normal”.

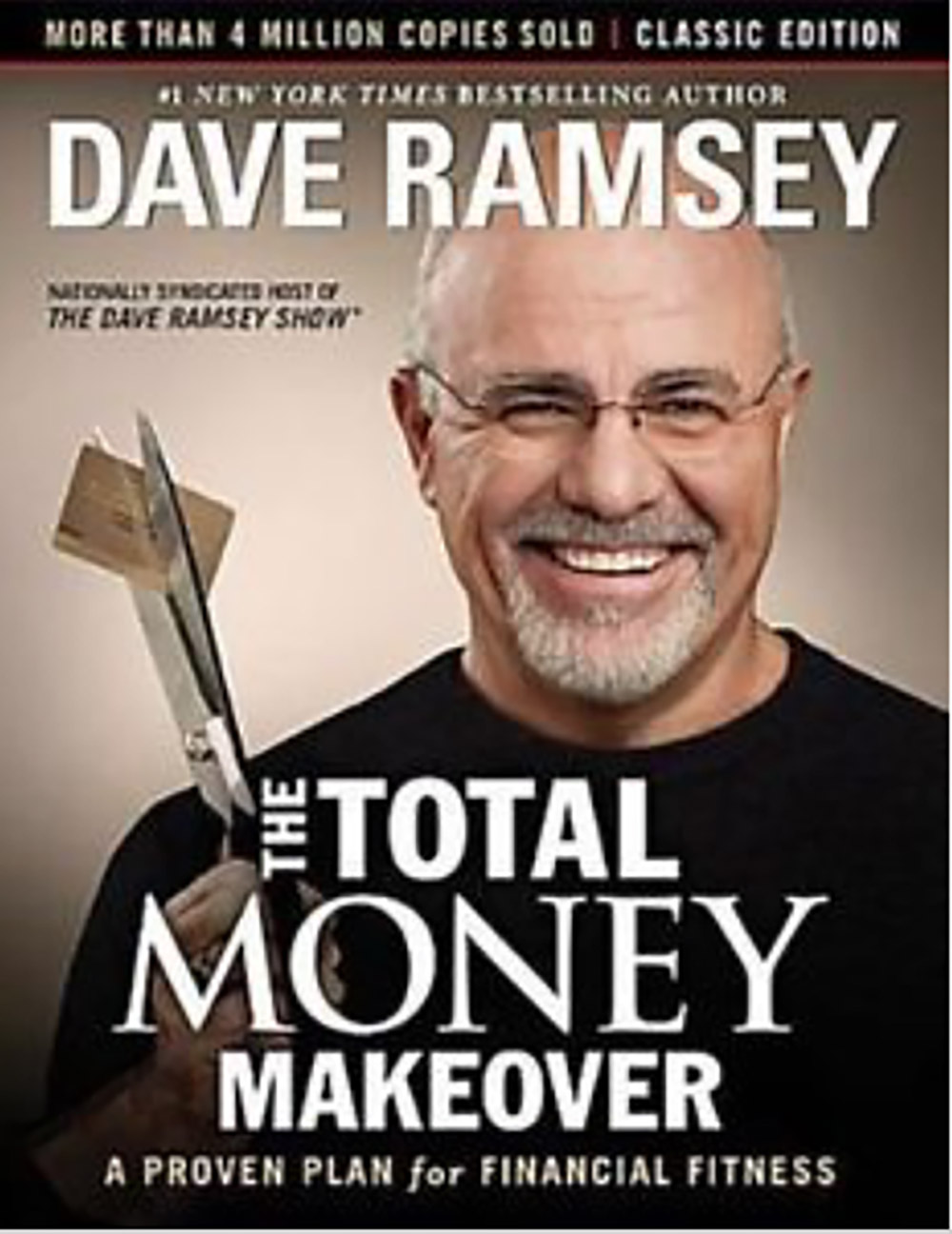

I’ve always been intrigued by the world of personal finance and have since dedicated the last two years to reading as much as I could on the topic. It wasn’t until three months ago that I got on a true real-numbers based budget and began to attack my debt using Dave Ramsey’s, Debt Snowball method. My advice for getting started is to assess your situation, then take action.

6 STEPS TO SUCCESS

1. Get your Credit Score and look at your Credit Report to see where you stand with the government and how you look to lenders during a credit analysis.

2. Pull out your bank statements and write down (in exact numbers) how much debt you owe. Numbers don’t lie and sometimes we have to get face to face with the truth before we can make an effective plan.

3. Get yourself on a BUDGET! None of this working with estimates stuff. What are your REAL numbers? What is your exact dollar amount of income and what bills and expenses do you have? Create a budget at the top of every month so that you can direct your dollars where to go. Why every month? Because expenses and income fluctuate. Cash gifts happen, doctors appointments get planned, and major life events happen that can change everything. Being prepared ahead of time, keeps you responsible and out of debt.

4. Quickly save $1,000 cash for emergencies. Stuff happens, I know. That’s how I ended up in debt. This eliminates the urge to charge a credit card or take out a loan for an emergency. For example, if you get in a car accident, most car insurance deductibles aren’t above $1,000. With the money saved, you can pay off the debt without charging a credit card. If your fund gets depleted, build it up again.

5. List your debts from smallest to largest and start paying off your debt one by one. Begin with the minimum payments on all of them and use excess money to pay down the smallest debt. When that debt is paid, take the minimum payment and the excess income and apply it to the next debt. This creates the debt snowball affect.

OR

5b. List your debts from the highest interest rate to the lowest, and pay your debt down that way. This one makes financial sense, but may be harder psychologically because your highest interest rate may be your largest debt. Therefore, it may be easy to lose steam because of the time it takes to build momentum.

6. Keep at it. Don’t give up! I’m currently on Dave Ramsey’s Baby Step Two and paying off my debt. It’s challenging, but I keep myself motivated with books, seminars, and podcasts. I’ll leave my favorite motivators below this video.

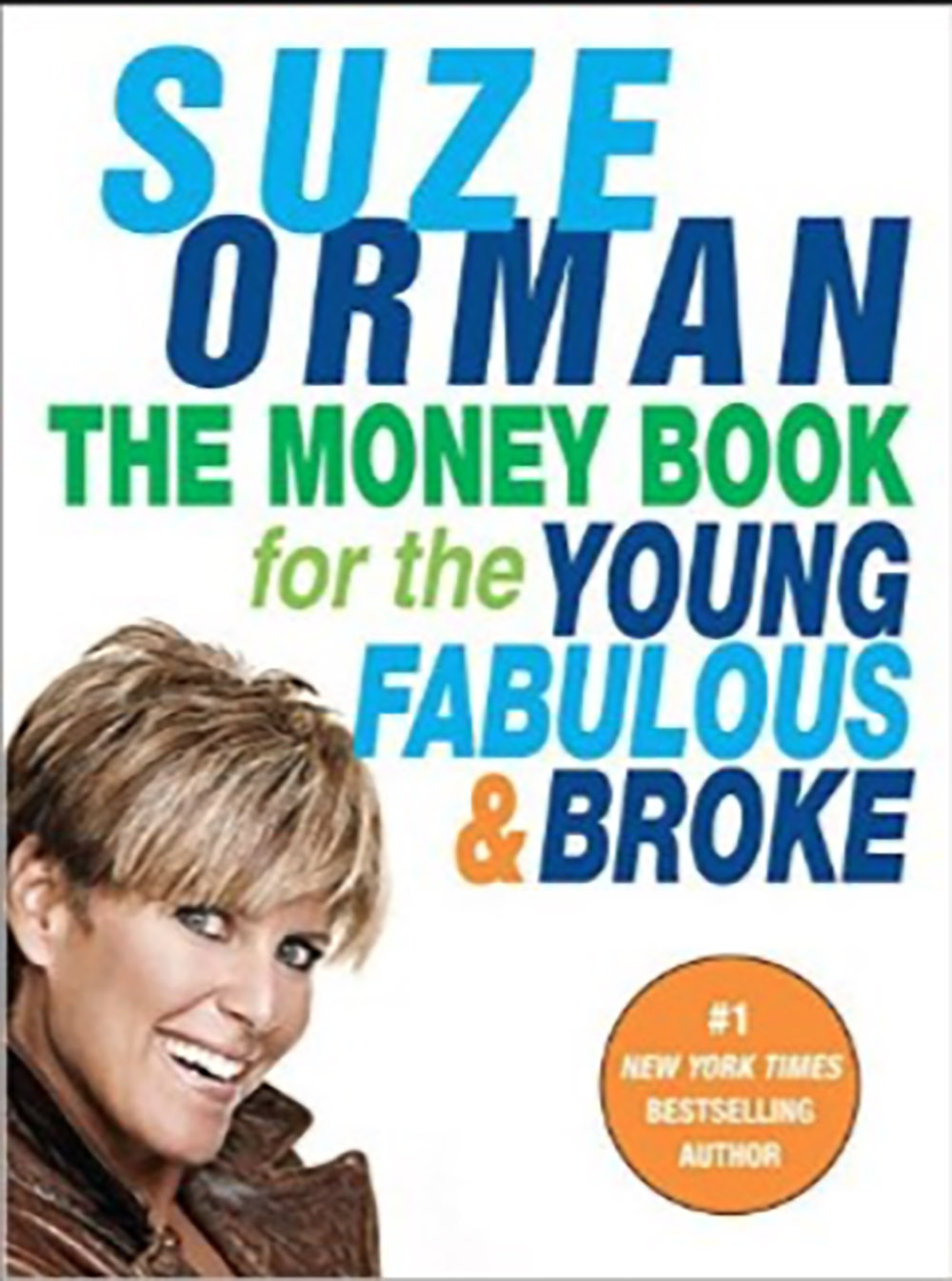

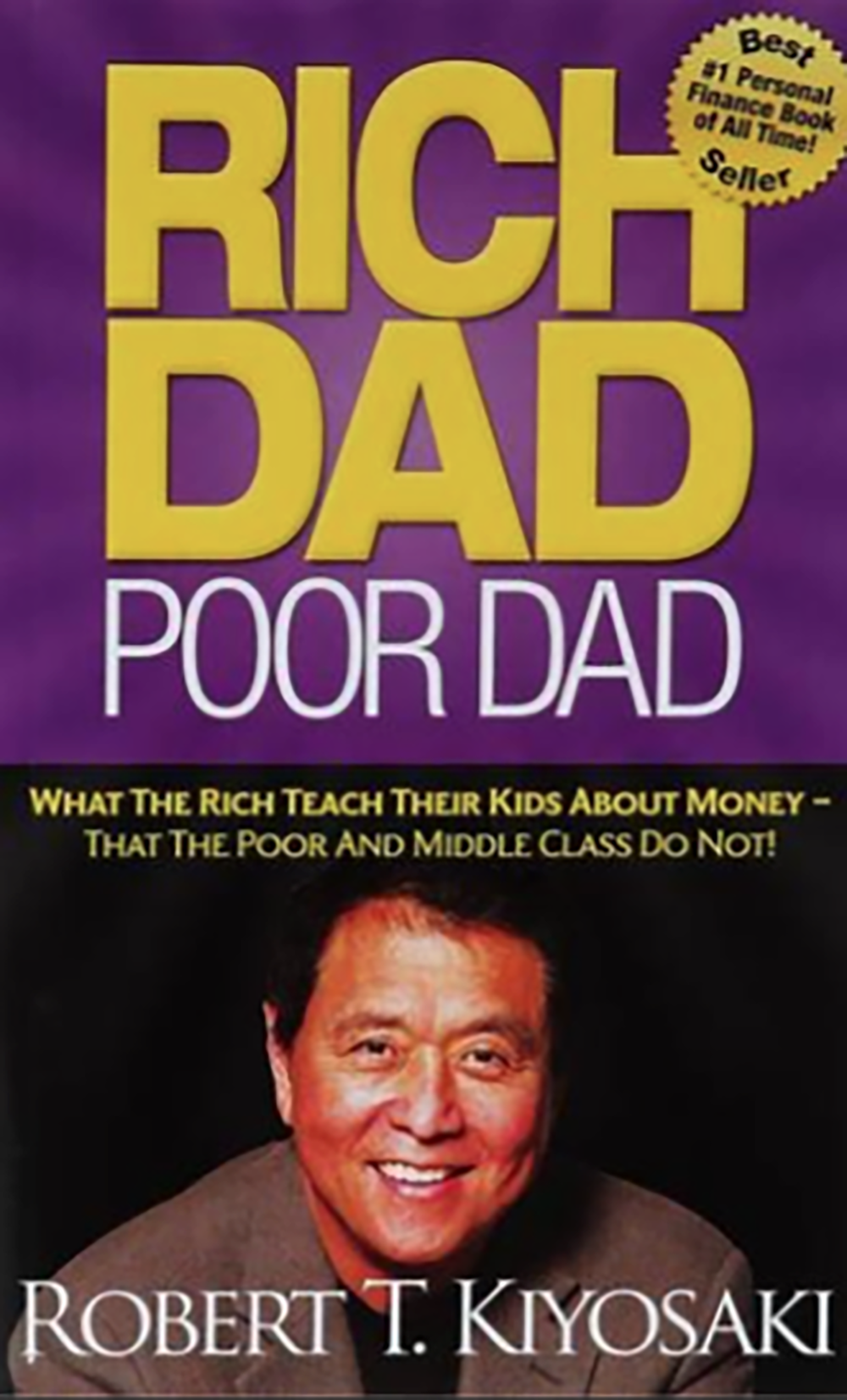

BOOKS TO GET YOU STARTED MANAGING YOUR MONEY

PODCASTS I LOVE

SO THERE IT IS

My first personal finance blog post! I hope my advice and suggestions help start you on your road to financial freedom. Happy debt destroying!